Foreword by CIO

Markets are adjusting to a world that is no longer defined by abundant liquidity, low inflation and frictionless globalisation. Instead, investors face a more complex backdrop of firmer inflation, evolving policy paths and rising geopolitical fragmentation.

Growth remains resilient but uneven, while central banks are likely to stay neutral rather than overtly supportive. At the same time, structural shifts in technology adoption, supply chain resilience and regional divergence continue to reshape the opportunity set. However, risks remain, particularly from a potential slowdown in capital expenditure and renewed inflation pressures from energy shocks, both of which could tighten financial conditions more abruptly.

Against this backdrop, our approach is focused on resilience over perfection: remaining invested, but with greater selectivity, diversification and a firm anchor in strategic asset allocation. I encourage you to speak with your Relationship Managers and Client Advisors for tailored guidance on positioning your portfolio for the evolving environment.

Thank you for your continued trust—we look forward to partnering with you through 2026 and beyond.

Dr Neo Teng Hwee

Chief Investment Officer and

Head of Investment Products and Solutions

UOB Private Bank

Overview

Key themes to watch

Agentic Artificial Intelligence (AI)

Agentic AI marks the shift from AI that answers questions to AI that executes tasks, positioning it as a new “digital workforce” for enterprises. While adoption is still early, accelerating ROI demand, improving cost dynamics, and a ready software ecosystem point to a long-term structural growth opportunity.

Strategic reindustrialisation

Strategic reindustrialisation reflects a structural shift from efficiency to resilience, as supply chains move from “just-in-time” to “just-in-case”. Driven by geopolitics, energy security and technological change, this multi-decade trend is reshaping global production and capital flows.

China: A tale of two markets

China equities are increasingly defined by a divergence between onshore and offshore markets, with A-shares benefiting from policy-driven growth in technology and industrial upgrading, while H-shares remain weighed by platform capex cycles and legacy sector exposure.

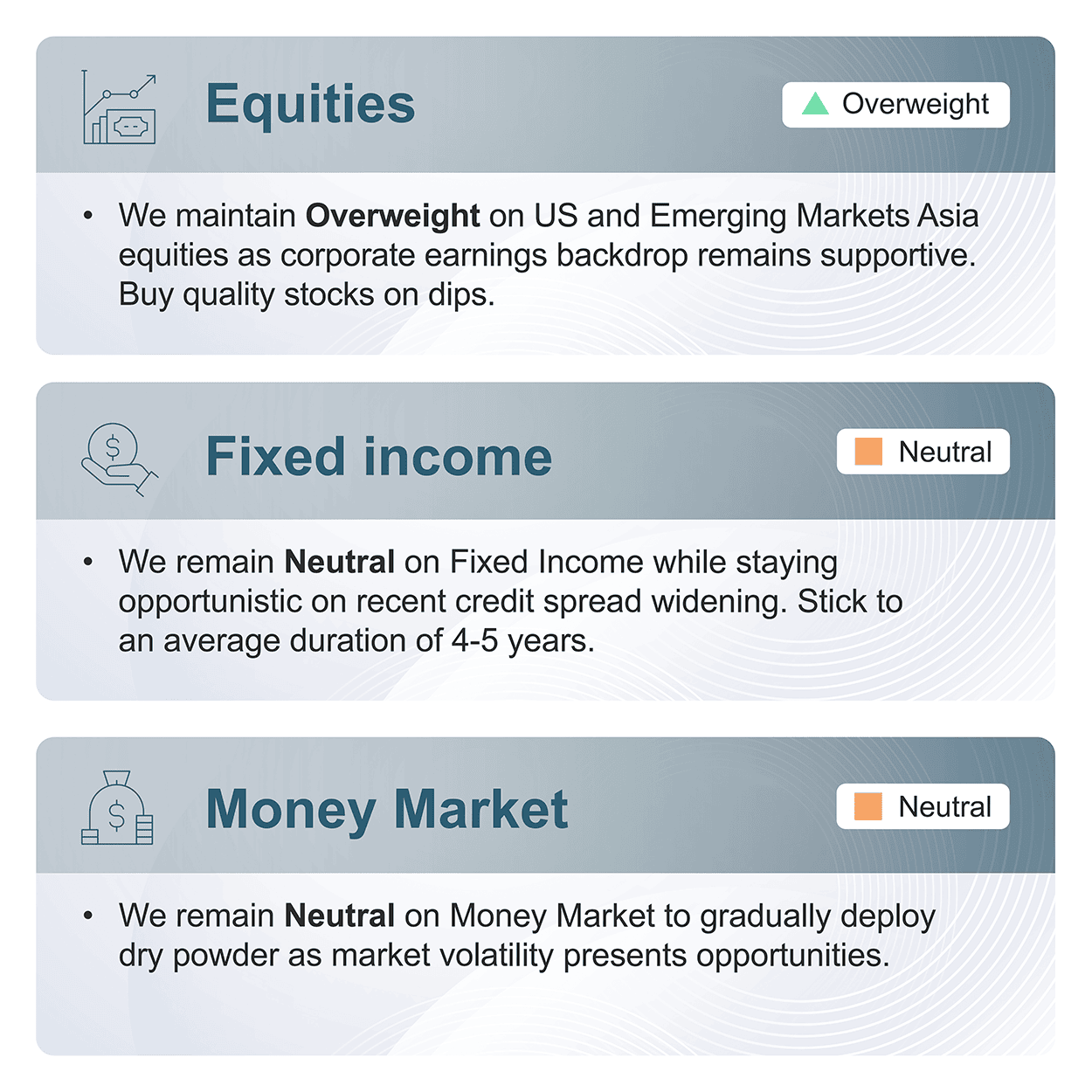

Asset allocation for 2H 2026

Additional Resources

Contact a UOB Advisor

Download Report

Get more investment insights

We use cookies to improve and customise your browsing experience. You are deemed to have consented to our cookies policy if you continue browsing our site.