The Travel Insider

Southeast Asia's first one-stop travel portal designed for UOB Cardmembers. Inspire, plan, and book your next adventure with UOB Cards.

Find out moreFeatured

Earn 2.5% p.a. interest on your Uniplus Account when you invest or insure with us.

Now enhanced to make your money work harder as you save and invest or insure with UOB. Subject to qualifying criteria. T&Cs apply. SGD deposits are insured up to S$100k by SDIC.

Find out moreCard Privileges

Cross over to your favorite deals in JB with UOB Cards

Tap your way to 0% FX fees, cashback on MYR spend and instant savings with UNI$ redemption.

Find out moreBorrow services

Balance Transfer

Get instant cash at 0% interest and low processing fees. Choose from 3, 6 and 12-months tenor.

Find out moreFeatured Solutions

Get early access to the JPMorgan Singapore & Asia Equity Income Fund

Tap into Singapore’s strengthening equities market while capturing Asia’s income & growth potential.

Learn more

UOB TMRW

Meet UOB TMRW, the all-in-one banking app built around you and your needs.

Bank. Invest. Be rewarded. Take charge with UOB TMRW.

-

you are in Personal Banking

For Individuals

Wealth BankingPrivilege BankingPrivate BankingFor Companies

GROUP WHOLESALE BANKINGGroup SME BankingForeign direct investmentUOB Asean insightsIndustry insightsSUSTAINABLE SOLUTIONSAbout UOB

UOB GroupBranches & ATMsSustainabilityTech Start-Up EcosystemUOB WorldUOB Subsidiaries

UOB asset managementUnited overseas InsuranceUOB travel plannersUOB Venture managementUOB Global capital

Guide to Submit Card Transaction Dispute

Notice an unrecognised transaction on your UOB Credit/Debit Card? Learn how you can report it.

What to do before raising a card transaction dispute:

Card Fee:

Are you referring to Card Annual Fee, Late Fee or Interest Charges instead? If so, please submit your request via Card Fee Waiver.

Merchant name:

Some merchants use a different name for payment processing. Check with merchants on the name used to reflect on cardholders’ statements.

Transaction date:

The transaction date on your card statement may differ from the actual date the purchase was made. This is normal if the merchant name and amount are correct. The date difference is usually due to late posting by the merchant or time zone differences for overseas transactions.

Supplementary cardholder:

Check whether the transactions were made by your supplementary cardholder or by family members who may have used your card.

Step 1: Lock your affected card via the UOB TMRW app

Launch the UOB TMRW app to lock your affected card. This will stop all new attempted transactions / payments immediately.

- Log in to UOB TMRW app

- Select the affected card

- Go to “Services” tab

- Tap on the “Lock card” icon

- Prompt is shown to confirm the request

- Tap “Lock now” to proceed

For more information on how to lock your card, please click here.

Step 2: Call our Call Centre Hotline to file for Disputes:

Please get the relevant information ready to provide to our Customer Service Officer. Please answer as factually as possible as this might impact your case outcome.

You will not be able to change the reason of the dispute request after your reporting.

- For Service Related: Call our dedicated 24/7 Hotline at 1800 222 2121

- For Dispute related: Call our dedicated 24/7 Fraud Hotline at 6255 0160

Reasons For Reporting a Transaction Dispute

1. Fraudulent Transactions

Report this if you see card transactions you did not make.

Examples:

- My card was lost or stolen

- I was scammed into making a payment

- My card details were exposed and misused

- I still have my card, but transactions are not mine (I did not perform the transaction)

2. Duplicate Charges

Report this if you were charged more than once for the same transaction.

Examples:

- Charged twice for the same goods or services

- Multiple charges for one ATM cash withdrawal

3. Issues With Goods or Services

Report this if there was a problem with what you ordered.

Examples:

- Goods or services did not arrive

- Goods were damaged or incorrect

- Services did not match what was ordered

- Cash received was not as requested

4. Cancelled Orders Still Charged

Report this if you cancelled an order but were still charged.

Examples:

- Refund not received after cancellation

- Charged instead of receiving a refund

- Recurring payment charged after cancellation

5. Other Transaction Problems

Report other issues related to a transaction you made.

Examples:

- Already paid using another method

- Charged in the wrong currency

- Charged the wrong amount

- Charged instead of receiving a refund

Our agent will assist in replacing your card after you have reported your disputed transaction. The card will be sent to your mailing address registered with the bank.

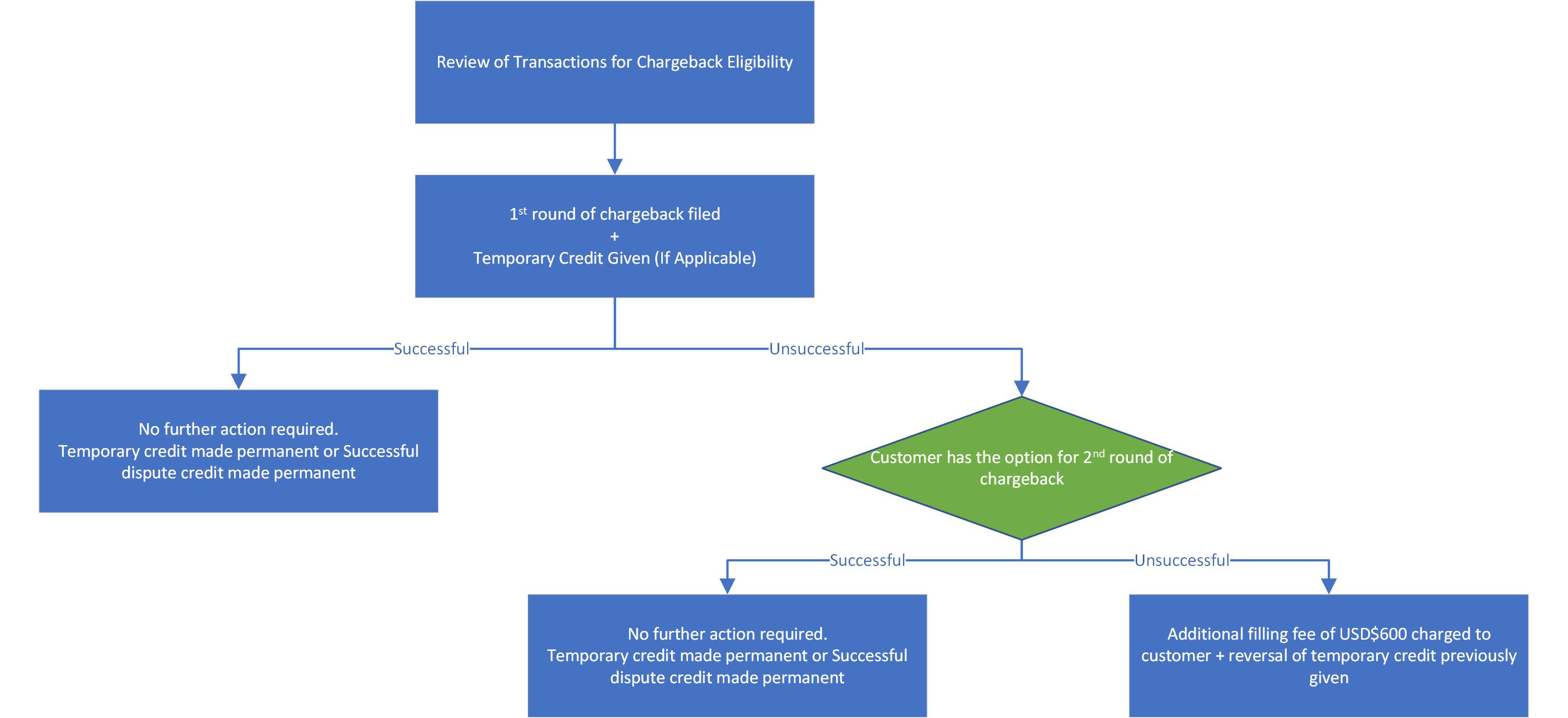

The Bank will review the disputed transaction against the respective Card Scheme rules and, while some transactions may not qualify for chargeback, we will make every effort to assist you in filing a chargeback with the Card Scheme, wherever possible.

We will also assess whether the disputed transaction is eligible for temporary credit. If eligible, temporary credit will be provided while we submit and manage the chargeback with the respective Card Scheme. The 1st cycle will take up to 50 calendar days.

If the outcome of the 1st round of the chargeback is unsuccessful, you may choose to proceed with the 2nd round of the chargeback. The 2nd round of the chargeback will take approximately 45 calendar days, but may take up to 180 calendar days or longer. Please note that if the final outcome from 2nd round of chargeback dispute is unsuccessful, there will be a filing fee of USD$600 payable to the respective Card Scheme and will be debited from your card account.

If the chargeback is successful at any stage, any temporary credit previously given will be made permanent. A permanent credit will be given if temporary credit was not provided earlier.

Terms & conditions may apply.

Safeguard your card by managing your card transaction alerts. You can take control of your cards anytime, anywhere by customizing its functions.

- Set your Card Payment Transaction Alert Threshold to $1.

- Temporary Block your card if you are not using it

Step 1 : Log in to UOB TMRW and tap "Accounts".

Step 2 : Select the affected debit or credit card you wish to block and report.

Step 3 : Go to “Services” tab, and tap on the “Lock card” icon.

Step 4 : There will be a prompt shown to confirm the request. Tap “Lock now” to proceed.

Step 5 : Review details and swipe right to confirm.

Step 6 : Your card has been locked! If you wish to unlock your card, you could tap on the “Lock card” icon on your card summary screen to unlock.

Step 7 : Tap on “Unblock card”.

Step 8 : Tap on “Next”.

Step 9 : Review details and swipe right to confirm.

Step 10 : Your card has been unblocked!

Transactions with a lower chance of chargeback success

While we always aim to support you, some transactions may be less likely to be successfully reversed under Card Scheme (VISA, MasterCard, American Express, UnionPay) rules. This is usually because the transaction was authenticated, authorised, or falls outside the scope of chargeback protection.

Below are common examples to help you understand when a dispute may have a lower likelihood of success.

Below are common examples to help you understand when a dispute may have a lower likelihood of success.

Important to know

- Each case is assessed individually based on card scheme rules

- Supporting documents play a critical role in dispute outcomes

- A dispute submission does not guarantee a refund

- Terms and conditions may apply

If you’re unsure whether your transaction qualifies, you can contact us and we can guide you on the appropriate next step.

FAQs (Frequently Asked Questions) for Card Transaction Dispute submission

We’re here to help

Help and support for your banking needs

Discover our Personal Banking FAQs

Explore our step-by-step guides

We use cookies to improve and customise your browsing experience. You are deemed to have consented to our cookies policy if you continue browsing our site.