You are now reading:

Top 5 scams in Singapore — and how to protect yourself against them

Southeast Asia's first one-stop travel portal designed for UOB Cardmembers. Inspire, plan, and book your next adventure with UOB Cards.

Find out more

Now enhanced to make your money work harder as you save and invest or insure with UOB. Subject to qualifying criteria. T&Cs apply. SGD deposits are insured up to S$100k by SDIC.

Find out more

Tap your way to 0% FX fees, cashback on MYR spend and instant savings with UNI$ redemption.

Find out more

Get instant cash at 0% interest and low processing fees. Choose from 3, 6 and 12-months tenor.

Find out more

Invest in funds powered by Private Bank CIO – United CIO Income Fund and United CIO Growth Fund.

Learn more

Meet UOB TMRW, the all-in-one banking app built around you and your needs.

Bank. Invest. Be rewarded. Take charge with UOB TMRW.

you are in Personal Banking![]()

You are now reading:

Top 5 scams in Singapore — and how to protect yourself against them

Good news: Scams in Singapore are declining. But members of the public can’t let their guard down just yet – scammers aren’t standing still, and it’s only a matter of time before they find new ways to exploit trust.

Based on UOB’s retail customer data and the Annual Scam and Cybercrime Brief 2025 from the Singapore Police Force (SPF), the public and private sectors' efforts to combat financial crime and scams in Singapore have been paying off.

UOB observed more than a 50% decrease in scam losses in 2025 compared with the previous year. Meanwhile, data from the SPF shows a 17.9% reduction in total amount lost to scams from S$1.1 billion in 2024 to S$913.1 million in 2025.

“UOB has strengthened its scam prevention framework by enhancing transaction monitoring, implementing targeted controls at key risk points, and working closely with industry partners and authorities. These measures are designed to support earlier detection and faster intervention to better protect our customers,” said Richard Soh, Executive Director, Anti-Fraud, Bribery & Corruption Policy, Advisory and Training, UOB.

The number of cases reported by UOB customers also declined by more than 20%. Nationwide, cases dropped from a peak of 51,501 cases in 2024 to 37,308 cases in 2025 (-27.6%). Yet that still represents a significant number of people and businesses affected by scams. To illustrate, that’s around 20 fully-loaded MRT trains of people affected by scams in 20251.

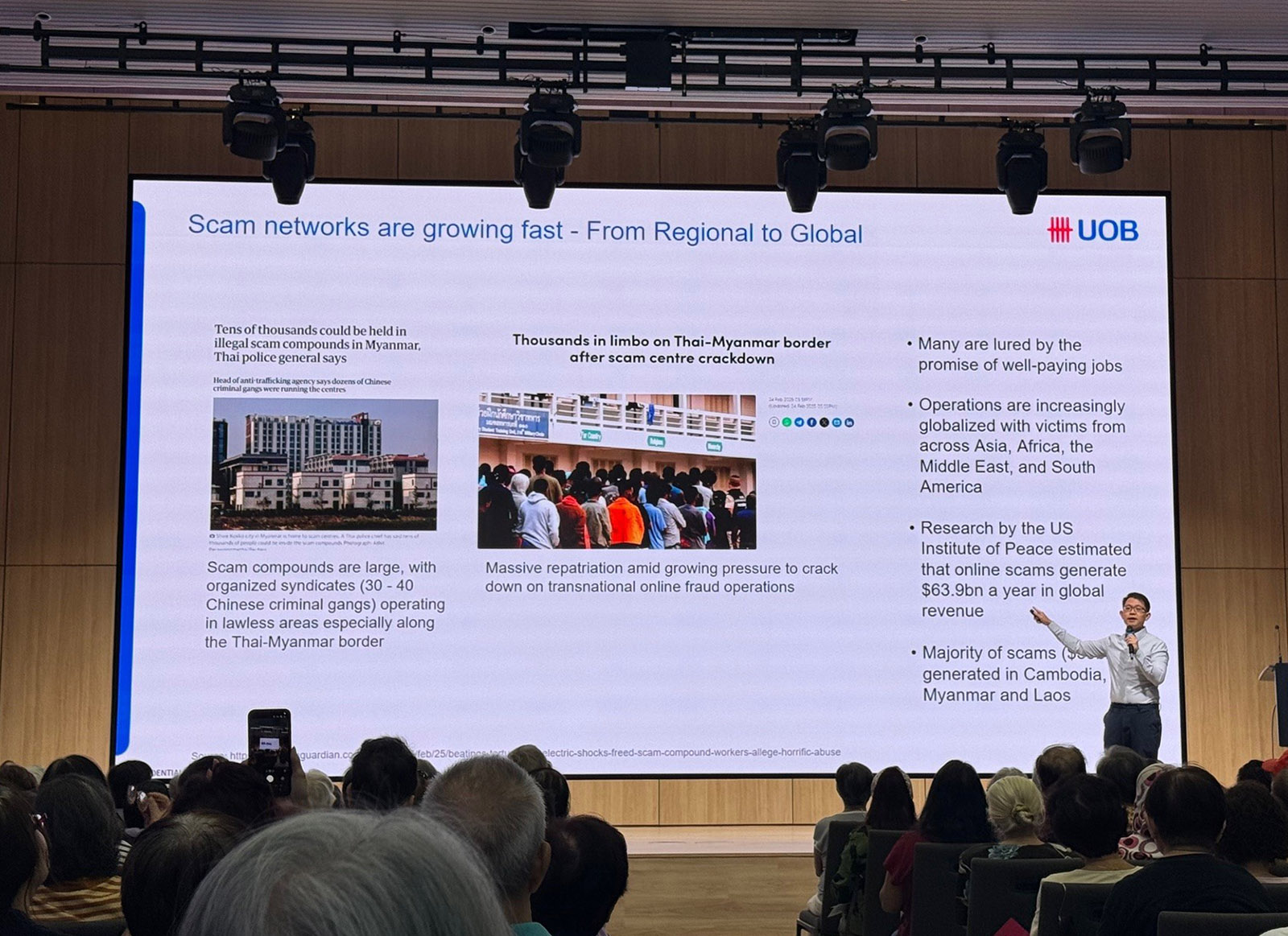

Some types of scams have grown more prevalent. In Singapore, Government Official Impersonation Scams (GOIS) more than doubled to 3,363 cases, with losses amounting to S$242.9 million. The 'always on' internet culture means younger people are falling prey to scams, too, especially e-commerce scams.

UOB’s data revealed the most common scam types affecting individual customers in 2025 are:

Meanwhile, the SPF’s data, which covers retail, business, and card fraud, found these to be the most common scam types in 2025:

It’s important to note that UOB and the SPF classify scam types differently, but both data sets show similar findings for general scam trends.

According to the SPF’s data, the majority (81.8%) of total reported scams had this in common: they were self-effected, meaning they were initiated, authorised, and completed by the account holder rather than a third-party. In other words, scammers manipulated victims into making money transfers themselves.

Next, we explore what each of these top scam types looks like, who normally falls for these scams, and the red flags or warning signs to look out for.

What are impersonation scams?

Impersonation scams are fraudulent attempts where scammers pose as authority figures, such as bank, financial, government, or police officers, to steal personal or financial information from victims. Scammers may create fake scenarios and use pressure tactics to create a sense of urgency, claiming victims need to pay ‘bail’ or ‘fines’ to trick them into sending the scammers money. Impersonation scams include Bank Officer Impersonation Scams (BOIS), Government Official Impersonation Scam (GOIS), and China Official Impersonation Scam (COIS)2. GOIS is one of the most common and ‘high loss’ scam types affecting Singaporeans, with losses increasing by 60.5% in 2025.

What do impersonation scams look like?

In recent cases, victims would receive unsolicited calls from scammers posing as representatives from insurance or financial institutions. They would claim that the victims had outstanding premiums and would then transfer them to scammers impersonating government officials from the Monetary Authority of Singapore (MAS) or the Ministry of Law (MinLaw). The victims would be accused of being involved in criminal activities and instructed to hand over their valuables for ‘investigation purposes’. The victims would only realise they had been deceived after the scammers became uncontactable.

Who gets affected by impersonation scams the most?

UOB data shows most impersonation victims are adults aged 50 and above, and the elderly (65 years and above), both in terms of the number of cases and the amount of money lost.

Last year, through the vigilance of UOB’s branch colleagues and the bank’s enhanced surveillance system, almost S$7.5 million in losses from impersonation scams were prevented, representing close to 50% of all losses averted.

What are the warning signs of an impersonation scam?

Signs of an impersonation scam include:

What are investment scams?

Investment scams involve scammers duping victims into fake investments by promising high returns with low risk. Scammers often lure victims through social media, messaging apps, or fraudulent investment websites, inviting them to participate in limited-time investment offers to create urgency. They may ask victims to send money or even cryptocurrency to unknown bank accounts, leading to significant losses. In 2025, S$336.2 million was lost to investment scams nationwide, accounting for 36.8% of total losses that year.

What do investment scams look like?

In some cases, scammers may add you to a chat group to learn about a new investment. For example, in February 2026, a victim was added to a WhatsApp group and presented with ‘investment opportunities’. The victim was instructed to download an app and to create an account. After experiencing technical difficulties, the victim was then directed by scammers to a helpline, which instructed the victim to hand over cash to an unknown man who identified himself as an authorised company representative for the victim’s investment. The victim lost more than S$8,000 to the WhatsApp scam.

The man was later arrested after trying to collect more money from the same victim for another investment.

Who gets affected by investment scams the most?

UOB data reveals that adults aged between 30 to 49 suffer the highest monetary losses from investment scams.

What are the warning signs of an investment scam?

Signs of an investment scam include:

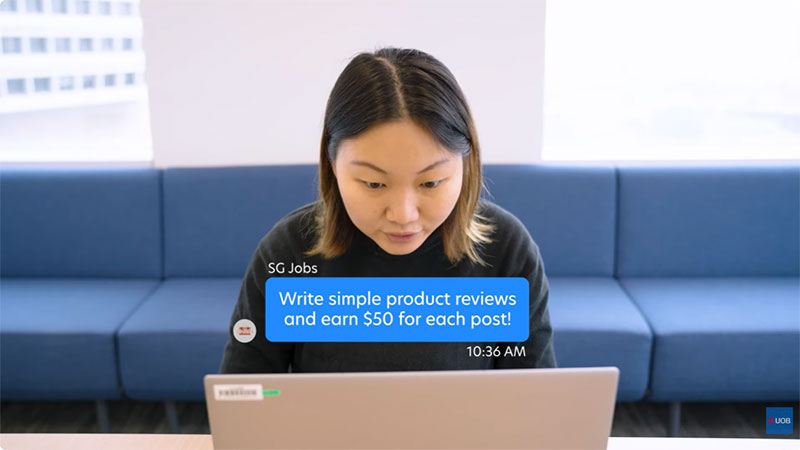

What are job scams?

Job scams involve scammers offering victims payment for fake, simple, and high-paying tasks they can perform online. For example, writing reviews, commenting on posts, or rating apps to boost product sales. Scammers may reach out via a messaging platform like Telegram, WhatsApp, or SMS, and request upfront payment or a deposit for ‘training’, ‘activation’, or miscellaneous fees before they can start work. The SPF observed that the number of job scams fell in 2025 to 5,575 (14.9% of total scam cases). However, they remain among the most common scam types with losses amounting to S$123.5 million in 2025, accounting for 13.5% of total losses.

What do job scams look like?

Victims of job scams have reported incidents when they would be contacted by scammers posing as human resources (HR) personnel from legitimate companies. They would reference active job listings and offer vague details about the company or the position to support their claims. Sometimes, they claim that the roles offered are on a ‘remote probation’ basis or require pre-paid fees as part of the hiring process, thus scamming victims into transferring money to them.

Who gets affected by job scams the most?

UOB data shows that young adults between 20 and 29 years of age are the most affected by job scams. This type of scam caused the second-highest financial losses for this age group, after investment scams.

What are the warning signs of a job scam?

Signs of a job scam include:

What are love scams?

Love scams in Singapore involve building an online relationship with the victim and manipulating them into buying gift cards or giving money, sometimes for emergency or investment purposes. These types of scams often occur on dating apps or social media platforms, where scammers use fake identities to build rapport with victims.

What do love scams look like?

Love scams can look like regular interactions on dating apps (e.g. Tinder, Bumble) or social platforms (e.g. Instagram, Facebook, Discord). But while they start out the same, love scams usually escalate quickly, with scammers building emotional intimacy and professing love within a short period of getting to know victims. After building trust, they may ask you for money or personal information, and cancel or postpone any opportunities to meet in person.

Some citizens reported receiving the same scripted message from people they matched with on dating apps.

Who gets affected by love scams the most?

UOB data shows love scams account for the second-highest losses for the elderly (65 years old and above), and third-highest losses for adults aged 50 to 60 years. However, with the rise of Generative AI and deep fakes, anyone can fall prey to realistic looking personas on video calls.

What are the warning signs of a love scam?

Some signs of a love scam include:

What are e-commerce scams?

E-commerce scams involve ‘fake sellers’ or ‘fake buyers’ who trick victims into making a payment online—often bypassing official merchant channels—with no intention of delivering the goods purchased. Nationwide, the number of e-commerce scams reported dropped 42.5% in 2025 compared with the year before, but it remains the most common scam type at 6,703 cases (18% of total scam cases), according to the SPF.

UOB data shows e-commerce scams are the third-most common scam type in 2025, typically causing smaller financial losses but across a larger number of cases.

What do e-commerce scams look like?

E-commerce scams look like typical listings for high-demand products or services, often at attractive prices, and listed on social media or fake websites. Instead of paying through an e-commerce platform’s secure payment channel, scammers will request direct payments or even crypto, or ask you to click on a phishing link or install a third-party app to complete the payment.

In February 2026, a man was arrested for falsely advertising pre-order sales of Pokémon trading cards on Telegram and cheating victims out of losses amounting to at least S$69,000. After the victims transferred money, the seller would become uncontactable.

Who gets affected by e-commerce scams the most?

UOB data shows youths (19 years old and below), young adults (20 to 29 years old), and adults (30 to 49 years old) fell prey to e-commerce scams more than any other type of financial scam in 2025.

What are the warning signs of an e-commerce scam?

Some signs of an e-commerce scam include:

If you receive a suspicious call, email, or message requesting you to transfer money, do these three things:

Always err on the side of caution. If something feels off, don’t act on it, even or especially if a stranger is pressuring you to do something.

“Scammers often rely on urgency and pressure. Customers can protect themselves by pausing to verify unexpected requests, being cautious about sharing personal or banking information, or they can contact UOB directly through official channels or visit any UOB branch if something feels wrong or suspicious,” added Soh.

While there are many different scam types, the tactics are usually the same. These are some of the red flags to look out for:

Look into the claims and who’s asking you to transfer money:

In January 2026, UOB was invited to speak at “Protect What Matters”, a scam awareness talk for more than 100 senior citizens, organised by Singapore Press Holdings (SPH) and sponsored by the Association of Banks in Singapore (ABS)

Prevention plays a critical role in tackling scams, especially since most scams stem from self-effected transfers, where individuals are tricked into authorising transactions themselves. This makes it even more important to put safeguards in place early, before funds are moved.

Banks like UOB are vigilant in preventing and intervening in potential scam cases. If you are a UOB customer, you can utilise UOB’s Money Lock to protect yourself.

UOB’s Money Lock feature lets you lock your savings to prevent unauthorised withdrawals. Money within the account will continue to earn the same interest.

You can set up Money Lock for some or all the funds in your existing savings account via the UOB TMRW app, UOB Personal Internet Banking, or any UOB ATM in Singapore. No additional fee is charged for using the Money Lock feature.

You can unlock your locked funds at any UOB ATM in Singapore, and they will be processed instantly. But for your security, your locked account cannot be removed or reduced via any digital means, phone banking, or any other regular UOB channels.

Alternatively, you can open a UOB LockAway Account to lock money you don’t need everyday access to.

UOB TMRW leverages data driven and AI enabled tools to provide personalised insights, which may help surface unusual patterns or activity within your accounts. Nevertheless, this does not replace customer’s own review of account activity. Thus, in addition to the above precautions, we encourage you to regularly review your account statements and remain vigilant at all times. Please do not share your banking credentials, one-time password or UOB TMRW screenshots with anyone.

At UOB, we work closely with partners like the SPF, National Crime Prevention Council (NCPC), and Infocomm Media Development Authority (IMDA) to prevent scams and raise awareness of scams among our customers. We also regularly hold scam talks with various Institutes of Higher Learning (IHLs), community centres and workplaces.

Be on guard and learn to avoid scams in Singapore. Protect your wealth and keep scammers away with Money Lock. Look out for our upcoming community events to learn more about how to prevent scams and manage your finances better.

1Based on a capacity of 1,800 people per MRT train. Source: SMRT

2Under UOB’s taxonomy, impersonation scams include fake friend scams but SPF tracks these cases separately.

This article is provided for general information purposes only and is not intended to constitute, and should not be relied upon as, financial, legal, investment, or other professional advice.

Information, examples, case studies, and statistics referenced in this article are based on publicly available data and UOB’s internal observations as at the date of publication, and may change from time to time without prior notice. UOB, its affiliates and their respective directors, officers and employees (collectively, the “UOB Group”) shall not have any obligation to update or revise such information to reflect subsequent developments, events, or circumstances.

Scam methodologies and financial crime tactics are constantly evolving, and accordingly, no information, tool, feature, service, or measure described in this article guarantees the prevention or detection of scams, fraud, or unauthorised transactions. Customers remain responsible for monitoring their accounts and exercising appropriate caution at all times. The UOB Group hereby shall not be responsible or liable for any loss, damage, cost or expense arising from or in connection with any reliance on the information contained in this article.

03 Nov 2025 • 5 min read

29 Oct 2025 • 5 MIN READ

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

Please refer to UOB Insured Deposit Register for a list of UOB accounts / products that are covered under the Scheme.